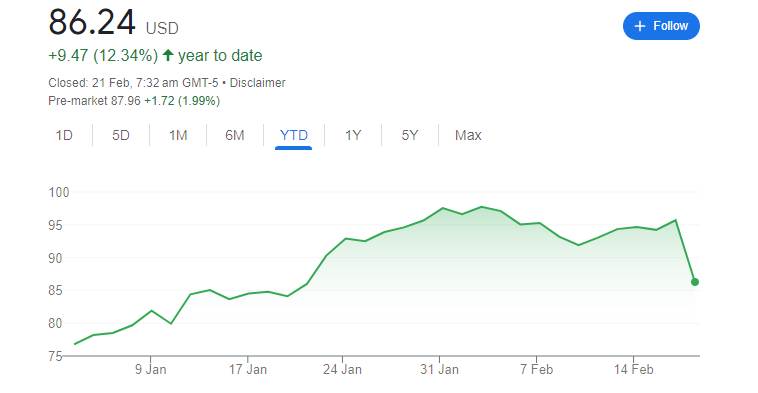

A major lithium stock, Stocks of Sociedad Quimica y Minera de Chile (NYSE: SQM), have increased 42% in the past year. But in our opinion, there is still plenty of value in this lithium stock.

SQM Is currently benefiting from a dramatic spike in the soft metal’s price. The business, SQM, has a sizable presence in Chile’s Atacama salt flats, where it uses a combination of chemical recovery and evaporation to extract lithium from brine.

Because it contains the greatest lithium concentrations ever recorded, Chile’s Atacama Desert is essentially the Saudi Arabia of the electric vehicle (EV) industry. The substance is an essential component of EV batteries.

Despite a strong 42% increase in the past year, the SQM share price is still $22 below its high of $111 in November.

Increased profitability and demand

Specialized plant nourishment, iodine, potassium, and chemical products make up the other four business sectors of SQM in addition to lithium. The business is the biggest producer of iodine, which is used in many medications and cleaning products.

This contributes to some profit diversification, but lithium is the greatest accomplishment. That’s because lithium prices began to rise in 2021 as a result of the world’s increasing demand for EVs and battery storage systems A Cambrian boom was consequently shown on the company’s income statement.

For the third quarter

| 2022 | 2021 | |

| Revenue from lithium | $2.33bn | $185m |

| Total revenue | $2.95bn | $661m |

| Net income | $1.09bn | $106m |

| Net income per share | $3.85 | $0.37 |

For the 9 months ended 30 September

| 2022 | 2021 | |

| Revenue from lithium | $5.62bn | $483m |

| Total revenue | $7.57bn | $1.77bn |

| Net income | $2.75bn | $263m |

| Net income per share | $9.65 | $0.92 |

Although the cost of lithium stocks has decreased this year, it is still much more than the five-year average. So, it comes as no surprise that the company has been making investments to improve its capacity for producing lithium. The majority of that is now finished, and the business anticipates growing its market share.

The management is open to additional acquisitions and has just acquired a refining facility in China. With more than $3 billion in cash on the balance sheet, it very certainly has the means to do so.

Cheap valuation with risk

The stock’s forward price-to-earnings (P/E) ratio is at 6.3. That means the shares may possibly be in a good price range at the moment when compared to the sector median of 14. The present dividend yield is astounding at 9%, with earnings covering it 1.8 times.

The benefit of accepting the chance that lithium stocks prices may decline further as additional supply enters the market is evidenced by this high yield. In 2024, Goldman Sachs projects that the average cost of lithium carbonate will be $11,000 a tonne. By comparison, the price would have decreased by more than 75%.

According to Macquarie Research, prices will remain stable through 2026 and average $62,586 per tonne in 2023. The average prediction is $29,063 per tonne for 2023.

Because of this variation, no one can say for sure. Yet, the global shift towards a greener economy should cause EV sales to increase tremendously over the long term. Lithium stocks demand is expected to increase 26-fold by 2050, according to the International Energy Agency, in order to achieve net zero.

The company’s profitability and dividend payments should remain stable as a result for many years. We would buy SQM stock today at a price of $86 per share if we hadn’t already done so.

Also read: Should You Purchase Lithium Stocks For Your Portfolio In 2023?